Ball Corporation is one of the world’s largest aluminum packaging companies, supplying aluminum beverage cans, bottles, and related sustainable packaging solutions to beverage, personal care, and household-product customers. In 2025, Ball generated $13.16 billion in net sales, shipped 111.9 billion aluminum packaging units globally, produced record comparable diluted EPS of $3.57, and generated record adjusted free cash flow of $956 million. The company also returned approximately $1.54 billion to shareholders through share repurchases and dividends during the year.

At first glance, Ball looks like a boring packaging company.

That is exactly why it is interesting.

Ball is not a software company, not an AI stock, not a hyped industrial-tech compounder, and not a biotech lottery ticket. It makes aluminum cans. Very, very many aluminum cans.

But after selling its aerospace business to BAE Systems in 2024 for $5.6 billion, Ball has become a much cleaner company. It is now effectively a pure-play global aluminum packaging business with improving volume growth, strong cash generation, disciplined capital returns, and a management team explicitly targeting 10%+ annual EPS growth.

The question for investors is simple:

Is Ball just a slow-growth packaging company, or is it a cash-generating aluminum packaging compounder hiding in plain sight?

Business Overview

Ball’s business model is straightforward but powerful. The company manufactures and sells aluminum packaging, primarily beverage cans, to global beverage and consumer-product companies.

Its customers include large brewers, soft-drink companies, energy-drink companies, sparkling-water brands, ready-to-drink cocktail producers, food and household-product companies, and emerging beverage brands.

The basic transaction looks like this:

- A beverage company needs aluminum cans for beer, soda, sparkling water, energy drinks, seltzers, or ready-to-drink beverages.

- Ball manufactures the cans in high-volume plants located close to customer demand.

- Ball passes through much of the aluminum cost through contractual pricing mechanisms.

- Ball earns margin from manufacturing efficiency, volume, mix, plant utilization, and customer contracts.

- The customer fills, distributes, and sells the finished beverage.

This is not a high-margin business, but it is a high-volume, high-scale, capital-intensive business where operational discipline matters enormously.

In packaging, small changes in volume, plant utilization, input costs, scrap rates, and logistics can meaningfully affect margins.

That makes Ball less like a commodity bet and more like an operating-execution story.

Strategic Shift: From Mixed Portfolio to Packaging Pure Play

Why this matters:

This graph shows the biggest strategic change in Ball’s story: after selling its aerospace business, Ball is now primarily an aluminum packaging company.

What it shows:

Before the aerospace sale, Ball had a more mixed identity: part packaging company, part aerospace supplier. After the sale, the company’s strategic identity is much cleaner.

Bottom line:

Ball is now easier to understand, easier to value, and easier for management to run. That simplicity matters.

Why the Aerospace Sale Matters

The sale of Ball Aerospace to BAE Systems was not just a divestiture. It changed the investment thesis.

Before the sale, Ball was a hybrid company with two very different businesses:

- Aluminum packaging

- Aerospace and defense systems

Those businesses had different customers, different cycles, different margins, different capital needs, and different valuation frameworks.

After the sale, Ball became much more focused.

The benefits are clear:

- simpler story

- cleaner financials

- more focused capital allocation

- less portfolio complexity

- more direct exposure to aluminum packaging demand

- greater ability to return capital to shareholders

But there is also a trade-off.

Aerospace was a high-quality business. Selling it removed diversification and left Ball more exposed to consumer packaging cycles, aluminum costs, and beverage demand.

So the sale improved strategic clarity, but it also increased reliance on execution in aluminum packaging.

That is the key nuance.

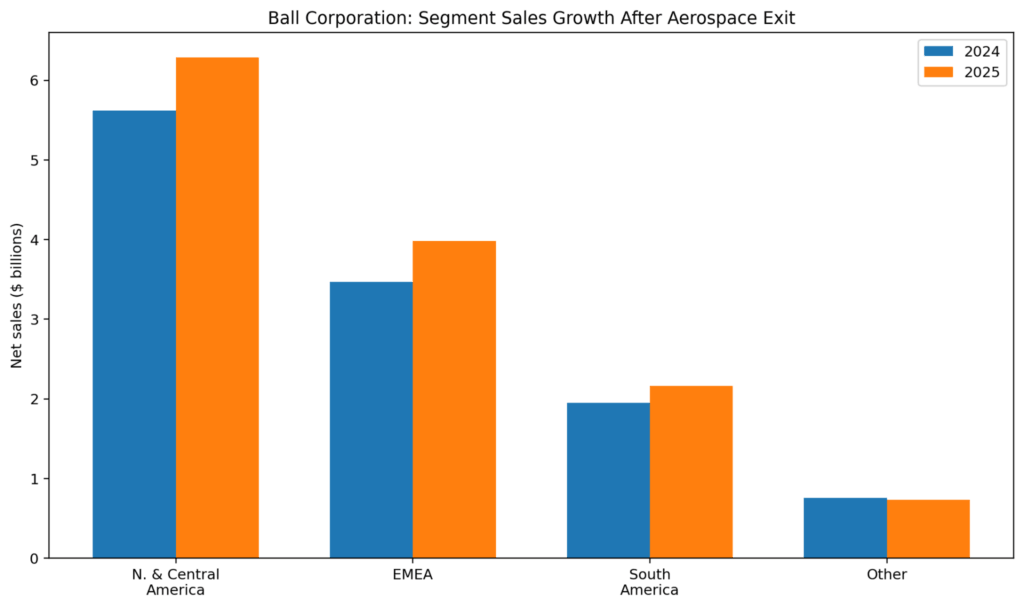

Segment Sales Growth

Why this matters:

This chart shows that Ball’s 2025 growth was broad-based across its major beverage packaging regions.

What it shows:

Ball’s North and Central America segment grew sales from $5.62 billion in 2024 to $6.29 billion in 2025. EMEA grew from $3.47 billion to $3.98 billion. South America grew from $1.95 billion to $2.16 billion. Other sales declined slightly from $759 million to $730 million due to portfolio actions and non-core changes.

Bottom line:

Ball’s 2025 growth was not concentrated in one region. The core beverage packaging business improved across major geographies.

Segment Breakdown

Ball reports three major beverage packaging segments:

Beverage Packaging, North and Central America

This is Ball’s largest segment and the most important profit pool.

In 2025, North and Central America generated approximately $6.29 billion in net sales and $772 million in comparable operating earnings. Segment volume increased 4.8% for the year.

This segment benefits from:

- beer

- soft drinks

- sparkling water

- energy drinks

- ready-to-drink cocktails

- customer scale

- strong plant network

- contractual aluminum pass-throughs

The North American market is mature, but it is still attractive because aluminum packaging continues to benefit from brand preference, sustainability positioning, and format innovation.

The risk is that North American beverage demand can be choppy. Beer demand has been pressured in some areas, and consumer spending can shift between at-home and away-from-home occasions.

Still, the region remains the backbone of Ball’s earnings base.

Beverage Packaging, EMEA

EMEA generated approximately $3.98 billion in net sales and $495 million in comparable operating earnings in 2025. Segment volume increased 5.5%, making it Ball’s fastest-growing major region by volume.

EMEA matters because it offers a combination of:

- volume growth

- sustainability-driven aluminum demand

- customer diversification

- geographic expansion

- improved operating leverage

Ball also completed the acquisition of an 80% stake in Benepack’s European beverage can businesses, including facilities in Belgium and Hungary, for approximately €184 million. This gives Ball more regional manufacturing capacity and strategic footprint in Western and Eastern Europe.

This is important because packaging is local. Cans are bulky and expensive to ship long distances. Having capacity near customers matters.

In packaging, geography is strategy.

Beverage Packaging, South America

South America generated approximately $2.16 billion in net sales and $327 million in comparable operating earnings in 2025. Segment volume increased 4.2%.

South America is smaller than North America and EMEA, but it has the strongest margin profile among the major reported segments.

This region benefits from:

- high can penetration

- beverage volume growth

- strong customer relationships

- favorable plant utilization

- regional operating efficiency

The key risk is macro volatility. South American markets can be more exposed to currency swings, inflation, political instability, and consumer purchasing-power pressure.

But from a margin standpoint, this is one of Ball’s most attractive regions.

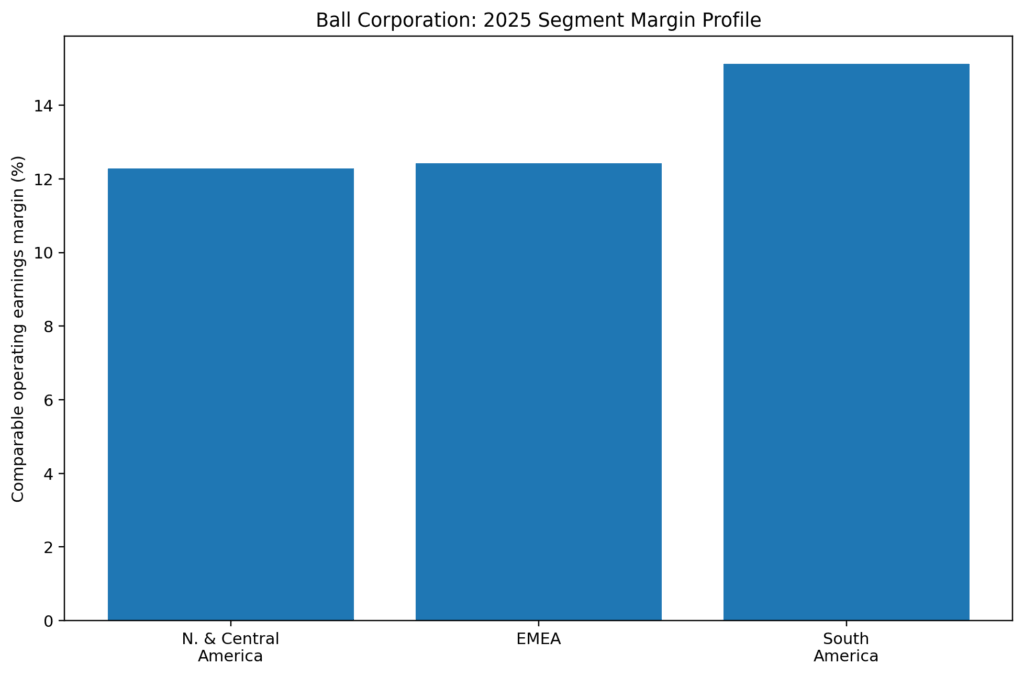

Segment Margin Profile

Why this matters:

Revenue growth is only half the story. This chart shows which regions convert sales into operating earnings most effectively.

What it shows:

South America has the highest 2025 comparable operating earnings margin among Ball’s major beverage packaging regions, followed by EMEA and North/Central America.

Bottom line:

Ball’s business is not equally profitable everywhere. Regional mix matters.

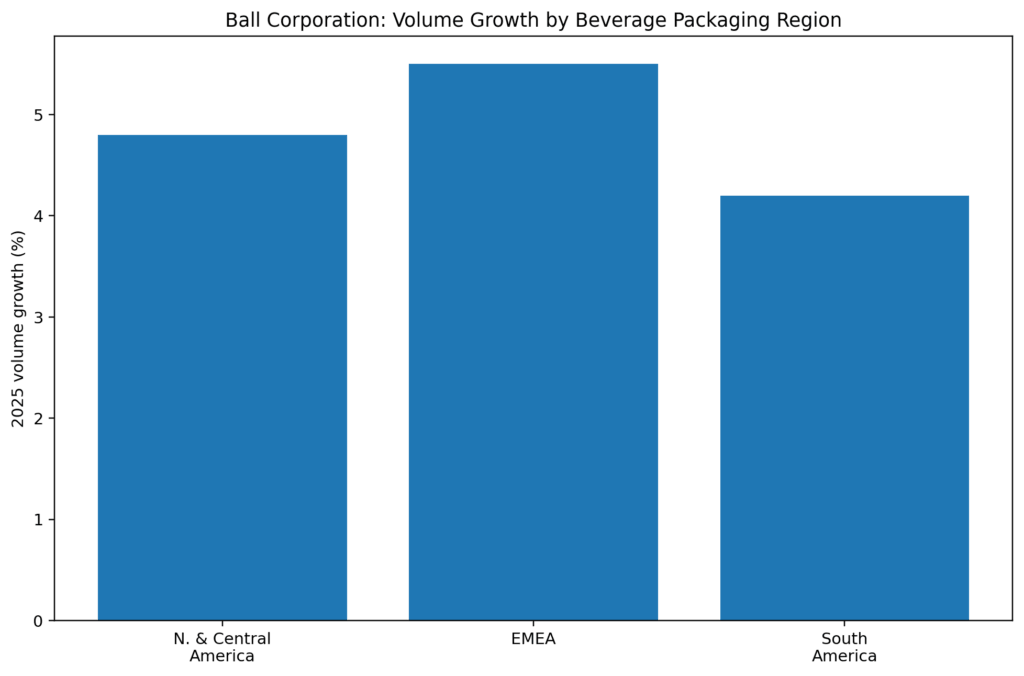

Volume Growth by Region

Why this matters:

Packaging companies are highly sensitive to volume. Volume growth improves plant utilization, spreads fixed costs, and supports operating leverage.

What it shows:

In 2025, Ball delivered positive volume growth across all major beverage packaging regions: 4.8% in North and Central America, 5.5% in EMEA, and 4.2% in South America.

Bottom line:

Ball’s earnings growth is not just price/mix. There is real unit-volume growth underneath the story.

Revenue Mechanics

Ball’s revenue is driven by five primary factors:

1. Unit Volume

The more cans Ball ships, the more revenue it generates. Volume also improves plant utilization, which matters because packaging manufacturing has significant fixed costs.

2. Aluminum Pass-Through

Aluminum is a major input cost. Many customer contracts include mechanisms that pass through aluminum-price changes. This helps protect Ball from raw aluminum volatility, although timing, regional premiums, tariffs, and working capital impacts still matter.

3. Price / Mix

Ball benefits when customers shift toward higher-value formats, specialty cans, resealable bottles, premium packaging, or new product categories.

4. Plant Utilization

A plant running efficiently at high utilization is much more profitable than one running below optimal capacity.

5. Geographic Mix

Regional margins differ. South America, North America, and EMEA do not all have the same profitability profile.

This is why Ball’s story is not simply “aluminum prices up or down.” The real driver is volume plus efficiency plus mix.

Cost Structure

Ball’s major costs include:

- aluminum

- coatings

- energy

- labor

- logistics

- plant maintenance

- depreciation

- freight

- working capital

- interest expense

The important point is that Ball is not purely exposed to aluminum like a miner or commodity trader. Much of the aluminum cost is passed through to customers, but Ball still faces:

- timing mismatches

- tariff effects

- regional premium changes

- inventory valuation swings

- customer pricing negotiations

- working-capital pressure

This creates a business that is partially protected from commodity swings but not immune to them.

Ball’s real operating edge comes from manufacturing discipline.

The company must:

- reduce scrap

- improve line speeds

- avoid downtime

- optimize freight

- manage labor

- keep plants full

- align capacity with customer demand

That is where the money is made.

Aluminum Packaging: Why It Still Matters

Aluminum cans are not exciting, but they are strategically advantaged.

They are:

- lightweight

- recyclable

- stackable

- durable

- fast to chill

- brandable

- widely accepted by consumers

- useful across beverage categories

Aluminum also benefits from sustainability positioning. Ball reported that 74% of the aluminum used by its global beverage packaging business in 2025 came from recycled sources. The company also shipped 111.9 billion aluminum packaging units worldwide.

This matters because consumer-packaged-goods companies are under pressure to reduce plastic exposure and improve packaging sustainability. Aluminum is not perfect, but it has a strong recycling story compared with many plastic formats.

That gives Ball a long-term demand tailwind.

The Sustainability Angle

The sustainability argument is one of Ball’s most important long-term demand drivers.

Brands care about aluminum because:

- consumers view it as recyclable

- it supports premium packaging formats

- it can replace some plastic packaging

- it works well for new beverage categories

- it offers strong shelf appeal

But sustainability alone is not enough.

Packaging decisions are still driven by:

- cost

- availability

- performance

- shelf life

- brand image

- logistics

- filling-line compatibility

So the bull case is not “aluminum is green, therefore Ball wins.”

The better argument is:

Aluminum has enough sustainability appeal, customer acceptance, and functional advantages to keep gaining share in selected beverage and consumer-packaged-goods categories.

That is more realistic and more investable.

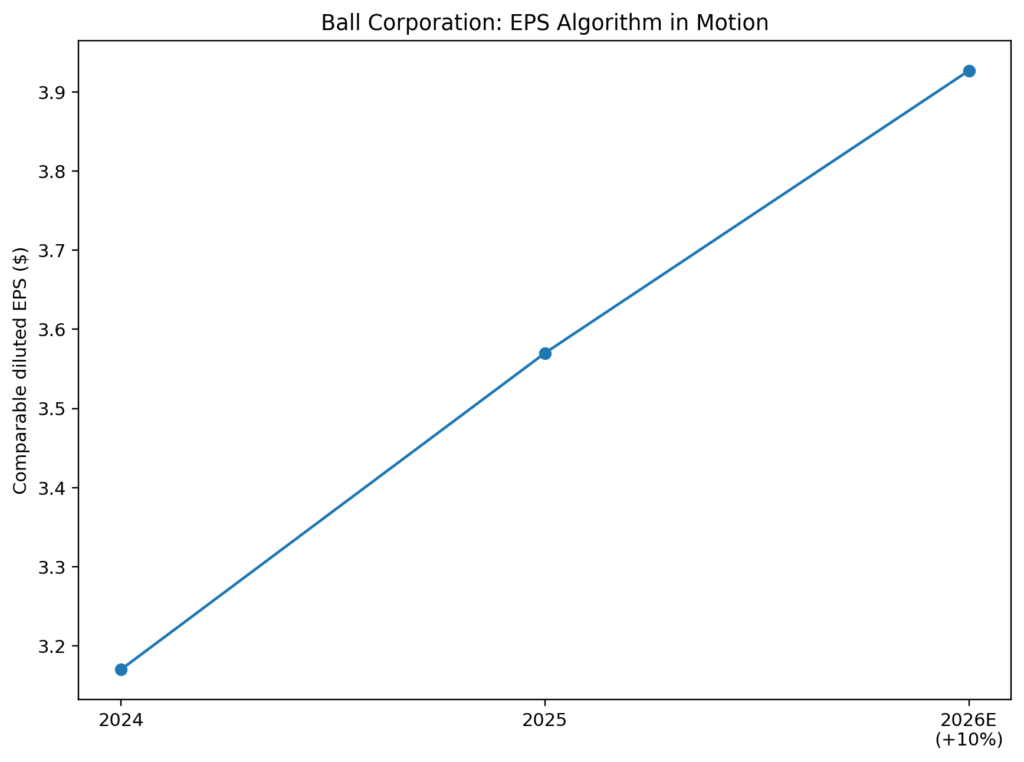

EPS Algorithm

Why this matters:

This chart shows the company’s earnings growth framework.

What it shows:

Comparable diluted EPS rose from $3.17 in 2024 to $3.57 in 2025. Management expects 10%+ comparable diluted EPS growth in 2026.

Bottom line:

The Ball thesis depends on whether management can consistently deliver the 10%+ EPS algorithm through volume growth, operating leverage, cost discipline, and capital returns.

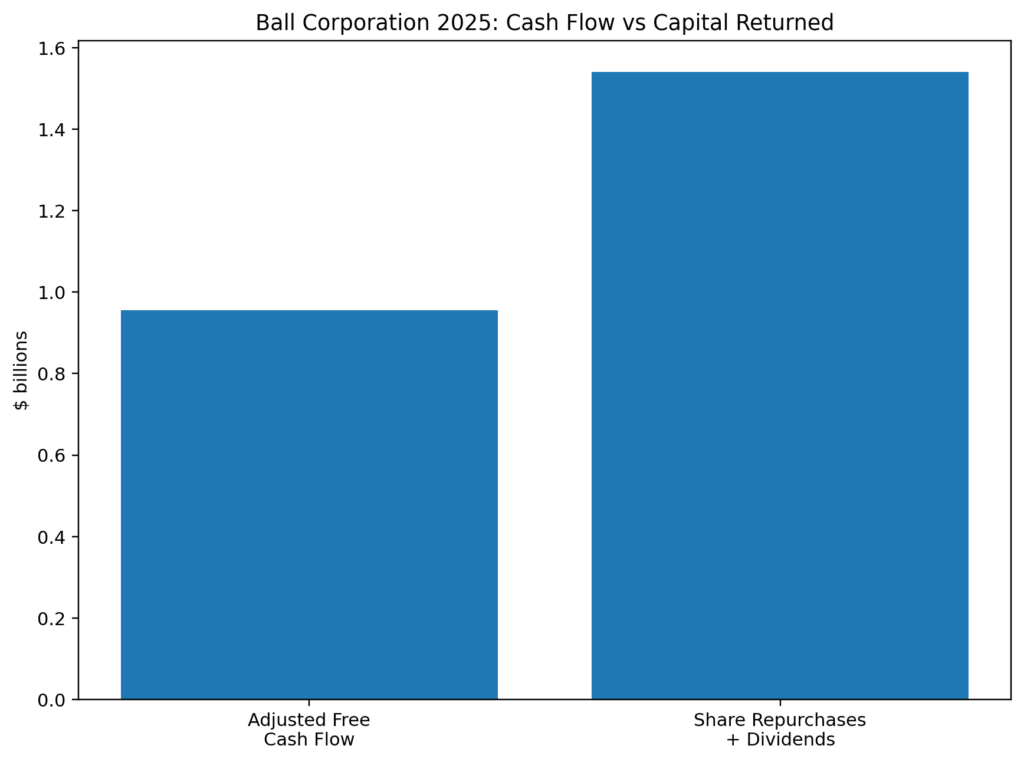

Cash Flow and Capital Returns

Why this matters:

This chart shows the tension and strength in Ball’s capital allocation story.

What it shows:

Ball generated record adjusted free cash flow of $956 million in 2025 and returned approximately $1.54 billion to shareholders through share repurchases and dividends.

Bottom line:

Ball is a cash-return story. But the company returned more capital than adjusted free cash flow in 2025, meaning investors should monitor leverage, buyback discipline, and balance-sheet flexibility.

Capital Allocation

Ball’s capital allocation strategy is central to the investment case.

The company has been returning capital aggressively through:

- share repurchases

- dividends

- disciplined capex

- portfolio actions

The aerospace sale gave Ball flexibility. In 2025, the company returned $1.54 billion to shareholders, far above its $956 million of adjusted free cash flow.

This is good if shares are undervalued and leverage remains manageable.

It is bad if buybacks are done too aggressively at the wrong valuation or if the company underinvests in growth capacity.

The right capital allocation balance is:

- invest enough to support profitable volume growth

- keep leverage reasonable

- return excess capital

- avoid empire-building acquisitions

- avoid overpaying for buybacks

Ball’s story works best if management behaves like rational capital allocators, not volume-at-any-price operators.

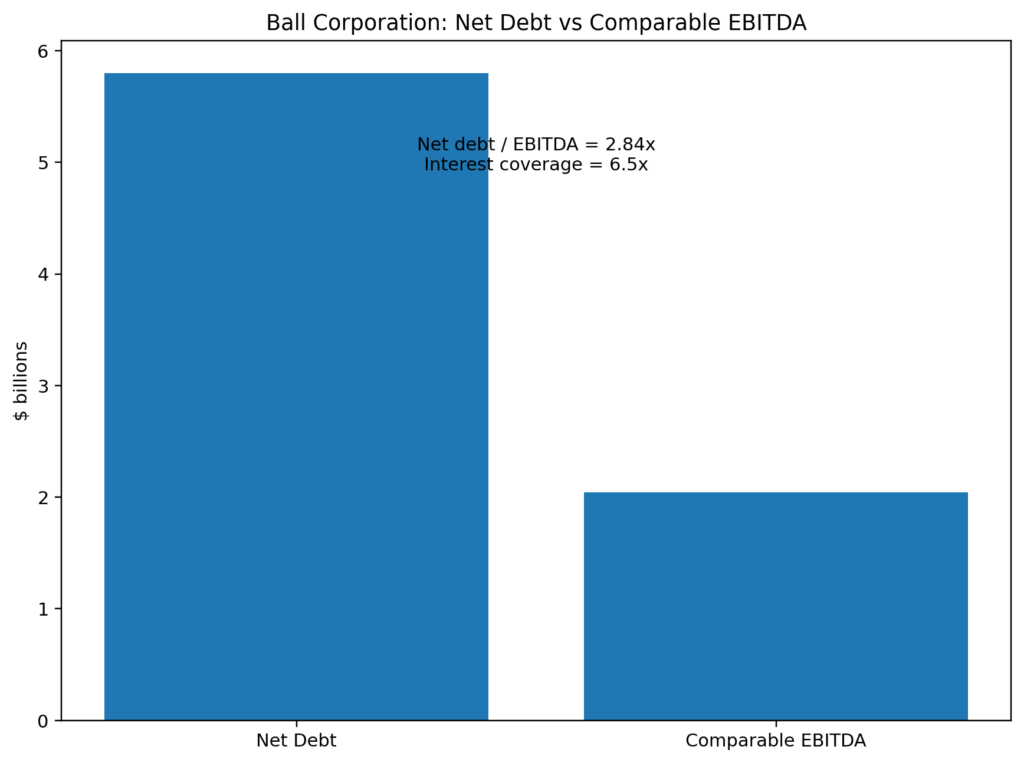

Balance Sheet and Leverage

Why this matters:

This graph shows Ball’s leverage position after the aerospace divestiture and capital returns.

What it shows:

Ball ended 2025 with approximately $5.8 billion of net debt, comparable EBITDA of approximately $2.04 billion, leverage of 2.84x, and interest coverage of 6.5x.

Bottom line:

Leverage is manageable, but not irrelevant. Ball has room to operate, but capital returns must remain disciplined.

Backdrop

Ball has gone through a major strategic reset.

The company:

- sold aerospace

- simplified the portfolio

- exited or deconsolidated certain non-core assets

- focused more tightly on aluminum packaging

- delivered record adjusted free cash flow

- grew global packaging volumes

- returned significant capital to shareholders

This is why the stock setup is interesting.

Ball is not a complicated sum-of-the-parts story anymore.

It is now a cleaner question:

Can a pure-play aluminum packaging company compound EPS at 10%+ while generating strong free cash flow and returning capital?

If yes, Ball deserves a solid multiple.

If no, it is just a cyclical packaging company with commodity/input-cost noise.

Why Now?

The timing is interesting for five reasons.

1. Portfolio Simplicity

After the aerospace sale, Ball is cleaner than it has been in years.

2. Volume Growth Has Reaccelerated

Global aluminum packaging shipments increased 4.1% in 2025, and all major regions posted positive volume growth.

3. Free Cash Flow Is Strong

Adjusted free cash flow reached a record $956 million in 2025.

4. Management Is Targeting 10%+ EPS Growth

The company’s 2026 outlook calls for comparable diluted EPS growth of more than 10%.

5. Capital Returns Are Meaningful

Share repurchases and dividends provide a direct shareholder-return mechanism.

The setup is not explosive. It is steady, operational, and compounding-driven.

That can be attractive if bought at the right price.

Stock Pitch: Ball Corporation (NYSE: BALL)

Executive Summary

Ball Corporation is a global aluminum packaging leader that has become significantly cleaner after selling its aerospace business. The company now offers investors exposure to aluminum packaging demand, sustainability-driven packaging trends, volume growth, operational execution, free cash flow generation, and aggressive capital returns.

This is not a high-growth story.

It is a cash-generating industrial packaging compounder.

Rating: Selective Buy / Accumulate on weakness

The stock is interesting because Ball now has:

- pure-play aluminum packaging exposure

- global scale

- positive volume growth

- strong free cash flow

- 10%+ EPS growth target

- meaningful capital returns

- manageable leverage

But it also faces:

- aluminum cost volatility

- tariff risk

- beverage demand cyclicality

- customer concentration

- packaging competition

- capital intensity

- valuation sensitivity

The stock works if Ball continues delivering volume growth, cost discipline, and buyback-driven EPS growth without stretching the balance sheet.

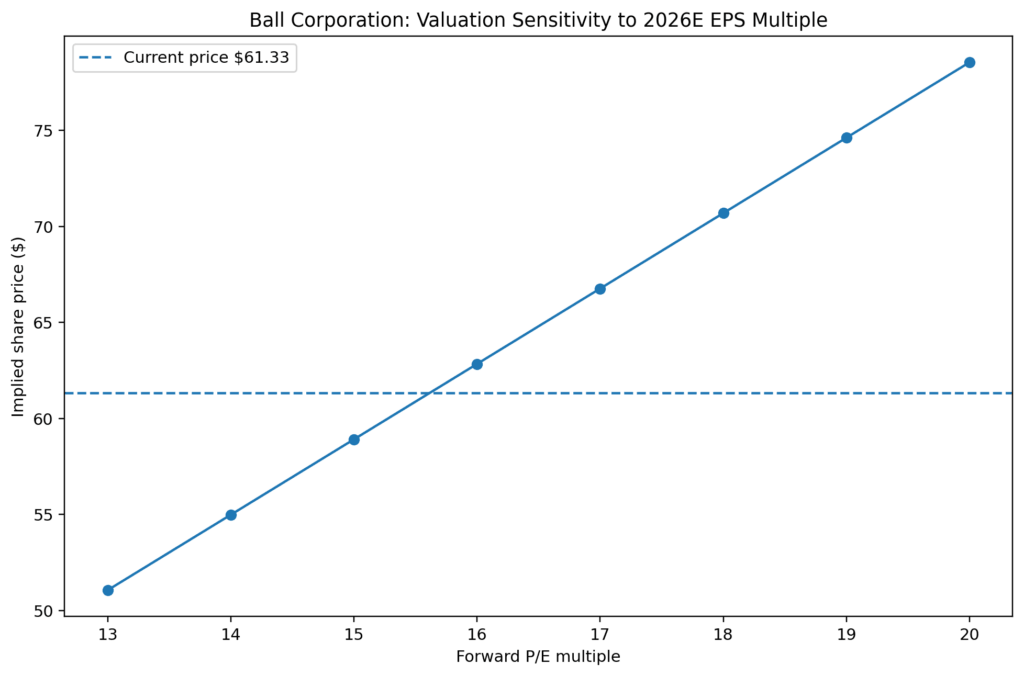

Valuation Sensitivity

Why this matters:

This chart shows how sensitive Ball’s share price is to the earnings multiple investors are willing to pay.

What it shows:

Using a 2026 comparable EPS estimate based on management’s 10%+ growth framework, Ball’s implied value changes materially depending on whether the market values the business at a low-teens, mid-teens, or high-teens earnings multiple.

Bottom line:

Ball’s upside depends on whether investors view it as a stable packaging compounder or just another cyclical container company.

Upside Drivers

1. Aluminum Packaging Volume Growth

Ball’s 2025 global aluminum packaging shipments increased 4.1%, with positive growth across North/Central America, EMEA, and South America. Continued volume growth is the cleanest upside driver.

2. Operating Leverage

Higher volumes improve plant utilization and spread fixed costs across more units.

3. Sustainability Tailwind

Aluminum’s recyclability supports long-term brand interest, especially as consumer-products companies look for alternatives to plastic.

4. Emerging Market Growth

Markets such as India remain underpenetrated and can grow faster than mature markets.

5. Capital Returns

Buybacks and dividends can support EPS growth and shareholder returns.

6. Portfolio Simplicity

The post-aerospace structure makes Ball easier to understand and potentially easier to value.

What Would Break the Thesis?

The thesis weakens if:

- beverage demand slows materially

- aluminum tariffs or regional premiums pressure customers

- Ball cannot pass through cost inflation effectively

- plant utilization declines

- emerging market growth disappoints

- customer concentration becomes a problem

- leverage rises due to aggressive buybacks

- EPS growth depends too heavily on financial engineering

- sustainability tailwinds fail to translate into actual volume growth

The biggest risk is that Ball becomes a buyback-driven packaging company rather than a true operating compounder.

Competitive Positioning

Ball competes with other packaging companies and container manufacturers, including Crown Holdings, Ardagh Metal Packaging, Canpack, Silgan, Amcor, and other regional producers.

Ball’s advantages include:

- global scale

- large customer relationships

- technical expertise

- manufacturing footprint

- recycled aluminum positioning

- strong beverage packaging focus

- operational know-how

Its disadvantages include:

- capital intensity

- exposure to beverage volumes

- input-cost volatility

- limited pricing power in some customer relationships

- dependence on large CPG and beverage customers

The key competitive point is that aluminum packaging is local, scale-driven, and operationally demanding. It is not easy to replicate Ball’s footprint quickly.

That gives the company durability.

What the Market Is Pricing In

At roughly $61 per share, Ball has a market capitalization of approximately $16.7 billion. The stock’s trailing P/E is about 22x, though forward valuation depends heavily on whether the company can deliver 10%+ EPS growth in 2026.

The market is pricing Ball as a decent, but not spectacular, packaging company.

Investors appear to recognize:

- better portfolio simplicity

- strong cash generation

- positive volume growth

- shareholder returns

But they may still be cautious because:

- packaging is cyclical

- aluminum costs are noisy

- beer and beverage demand can be uneven

- capital intensity limits free cash flow flexibility

- much of the aerospace-sale benefit is already behind the company

This creates a balanced setup.

Ball is not obviously cheap, but it is also not being valued like a premium industrial compounder.

Current Market Sentiment

The market currently views Ball as:

- a cleaner company post-aerospace sale

- a leading aluminum packaging platform

- a cash-flow and buyback story

- a beneficiary of sustainability trends

- but still a cyclical packaging business

That distinction matters.

Ball is better than a generic commodity packaging company, but it is not immune to packaging cycles.

What Needs to Go Right

For the stock to work, several things need to happen:

- global can volumes must continue growing

- plant utilization must remain healthy

- cost pass-through mechanisms must hold

- management must hit 10%+ EPS growth

- free cash flow must remain strong

- buybacks must be disciplined

- leverage must stay manageable

- sustainability tailwinds must show up in actual shipped units

The thesis is measurable. Watch shipments, margins, free cash flow, leverage, and buyback discipline.

Why the Opportunity Exists

The opportunity exists because Ball is easy to underestimate.

It sounds boring.

It makes cans.

But boring can be beautiful when the company has:

- global scale

- recurring customer demand

- manufacturing expertise

- free cash flow

- capital returns

- simplified portfolio

- sustainability tailwinds

The stock does not need a huge narrative. It needs execution.

That is why Ball is interesting.

Bottom Line

Ball Corporation is no longer a mixed packaging and aerospace company. It is now a cleaner global aluminum packaging pure play.

The company has:

- $13.16 billion in 2025 net sales

- 111.9 billion aluminum packaging units shipped

- record comparable EPS

- record adjusted free cash flow

- strong shareholder returns

- positive volume growth across major regions

- a clear 10%+ EPS growth target

The risk is that investors overpay for a packaging company that remains exposed to input costs, beverage cycles, and customer concentration.

The opportunity is that Ball may be a better business than the market gives it credit for: not glamorous, but scaled, cash-generative, operationally focused, and increasingly simple.

This is not an exciting stock.

That may be the point.

Sometimes the best businesses are the ones nobody brags about owning.

DISCLAIMER

This analysis is not investment advice and reflects opinion only.

© 2026 MacroHint.com. All rights reserved.

This article is proudly sponsored by Lake Region State College.

Michael Lazenby

Michael Lazenby is the Editor-in-Chief and Founding Partner of MacroHint. He studied economics, business, and government at UT Austin and has hedge fund experience.

Michael Lazenby is the Editor-in-Chief and Founding Partner of MacroHint. He studied economics, business, and government at UT Austin and has hedge fund experience.