Camden Property Trust is a large U.S. multifamily REIT focused on owning, operating, acquiring, developing, and redeveloping apartment communities. Camden owns and operates over 58,000 apartment homes across major U.S. markets, with a heavy concentration in high-growth Sun Belt regions.

Camden is not a high-growth narrative stock. It is a high-quality real estate platform currently working through a difficult supply-driven apartment cycle. The key question is whether the market is over-discounting near-term rent pressure and underappreciating long-term fundamentals.

At its core, Camden today is a multifamily reset story: weak new lease pricing, strong occupancy, stable cash flow, and a setup that improves meaningfully if supply normalizes.

Business Overview

Camden generates revenue by leasing apartment units and collecting rent. Its performance is driven by:

- Occupancy

- Effective rent per unit

- New lease rates

- Renewal lease rates

- Same-property NOI growth

- Development completions

Costs are driven by:

- Property taxes

- Insurance

- Maintenance

- Payroll

- Utilities

- Interest expense

The key issue today is not demand destruction—it is oversupply in key Sun Belt markets, which has reduced pricing power.

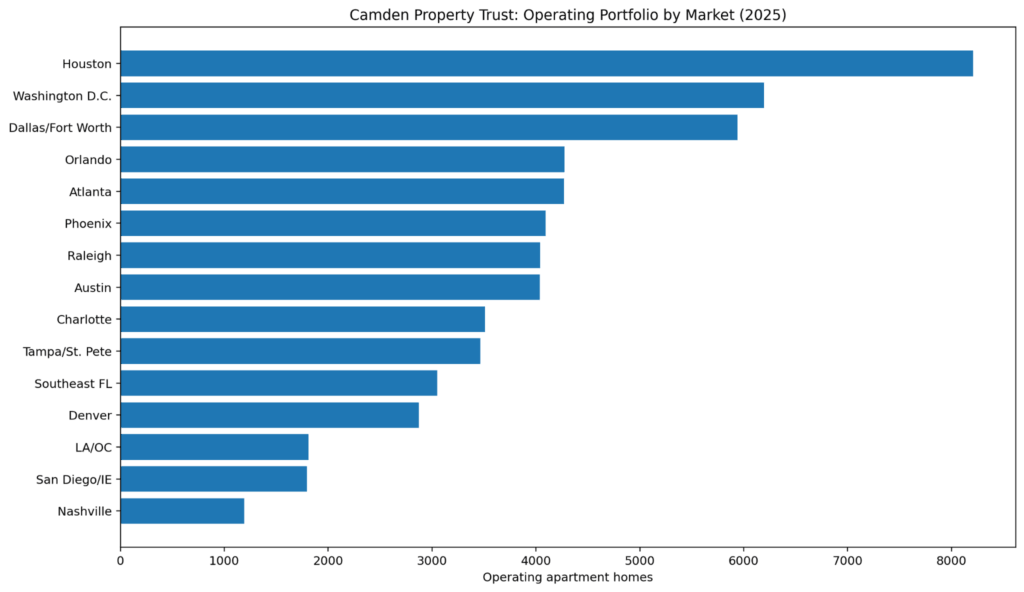

Camden Portfolio by Market

Why this matters:

This shows exactly where Camden is exposed. The portfolio is concentrated in Sun Belt and high-growth metro areas like Houston, Dallas, Orlando, Atlanta, Phoenix, and Austin.

What it shows:

Camden is highly levered to migration trends, job growth, and long-term housing demand—but also exposed to near-term supply pressure in those same markets.

Bottom line:

If Sun Belt supply normalizes, this geographic exposure becomes a tailwind again.

Revenue Mechanics

Camden’s earnings come from three buckets:

Stabilized Portfolio

The core business—existing properties generating recurring rent income. This is where occupancy, rent growth, and expense control matter most.

Development Pipeline

New construction projects that temporarily dilute earnings during lease-up but can create long-term value if built at attractive yields.

Capital Recycling

Selling older assets and redeploying capital into acquisitions, development, or share repurchases.

Lease Trade-Out Dynamics (Core Issue)

Why this matters:

This is the most important operating chart in the entire article.

What it shows:

- New leases are negative

- Renewal leases are still positive

- Blended lease growth is slightly negative

This means:

- Camden is maintaining occupancy

- But losing pricing power on new tenants

Bottom line:

This is not a demand problem—it’s a supply problem.

Cost Structure & Margin Pressure

Even with stable occupancy, Camden is seeing:

- Low revenue growth

- Higher expense growth

- Flat to declining NOI

This compresses operating leverage and limits earnings growth.

The issue is timing: costs adjust faster than rents recover.

Cash Flow and Dividend Coverage

Why this matters:

This shows whether Camden can sustain its dividend.

What it shows:

- Core FFO remains stable

- AFFO supports the dividend

- Dividend is well-covered

Bottom line:

The dividend is not at risk—the issue is growth, not stability.

Development Economics

Why this matters:

This breaks development down to the unit level.

What it shows:

Different projects have materially different cost bases per apartment home. This determines whether development creates value or destroys it.

Bottom line:

Development only works if future rents justify today’s construction costs.

Backdrop

The apartment market is currently digesting a large wave of new supply, especially in Sun Belt markets.

This creates a paradox:

- Occupancy remains high

- Rent growth weakens

Camden’s guidance reflects this:

- Flat to slightly down FFO

- Weak NOI growth

- Continued near-term pressure

The market is reacting to this by compressing valuation.

Why Now?

The opportunity exists because:

- The market sees weak rent growth

- The market sees negative lease spreads

- The market sees flat earnings

But:

- Occupancy is strong

- Cash flow is stable

- The portfolio is high quality

- Supply is cyclical, not permanent

The key question:

Is 2026 the trough?

Stock Pitch: Camden Property Trust (NYSE: CPT)

Executive Summary

Camden is a high-quality multifamily REIT trading through a cyclical downturn.

This is not a momentum story. It is a cycle timing story.

Rating: Selective Buy / Accumulate

Valuation Sensitivity

Why this matters:

This shows how sensitive the stock is to valuation multiples.

What it shows:

Even modest changes in FFO multiple result in meaningful price changes.

Bottom line:

Upside is driven more by multiple expansion than earnings growth.

Upside Drivers

1. Supply Normalization

As new construction slows, pricing power returns.

2. Lease Stabilization

New lease declines bottom and begin improving.

3. Strong Occupancy

High occupancy supports revenue base.

4. Capital Allocation

Share buybacks and asset recycling add value.

5. Development Optionality

Projects deliver value in a better rent environment.

What Would Break the Thesis?

- Continued negative new lease rates into 2027

- Renewal rates turning negative

- Expense growth exceeding revenue growth long-term

- Extended oversupply in key markets

- Higher-for-longer interest rates compressing REIT multiples

This is not a balance sheet risk—it is a duration risk.

Competitive Positioning

Compared to peers:

- Coastal REITs have less supply pressure

- Sun Belt REITs (like Camden) have more growth—but more volatility

Camden sits in the middle:

- Strong long-term markets

- Weak near-term fundamentals

Capital Allocation

Camden is actively:

- Buying back shares

- Recycling capital

- Developing selectively

This is important because management is not passive—they are actively managing through the cycle.

Management Overview

Camden is known as a disciplined operator with a long-term focus on:

- balance sheet strength

- market selection

- capital allocation

This is not a company reacting to crisis—it is managing through a cycle.

Current Market Sentiment

The market currently views Camden as:

- A good company

- In a bad part of the cycle

That distinction is critical.

What the Market Is Pricing In

Why this matters:

This reframes the entire investment case. Instead of asking what Camden could earn, this asks what the market already assumes it will earn.

What it shows:

At current valuation levels, the market is effectively pricing in low long-term rent growth, roughly in the ~1–2% range. That is below historical multifamily growth in Camden’s core markets.

Bottom line:

You do not need strong growth for this to work—you just need outcomes to be less weak than currently priced in.

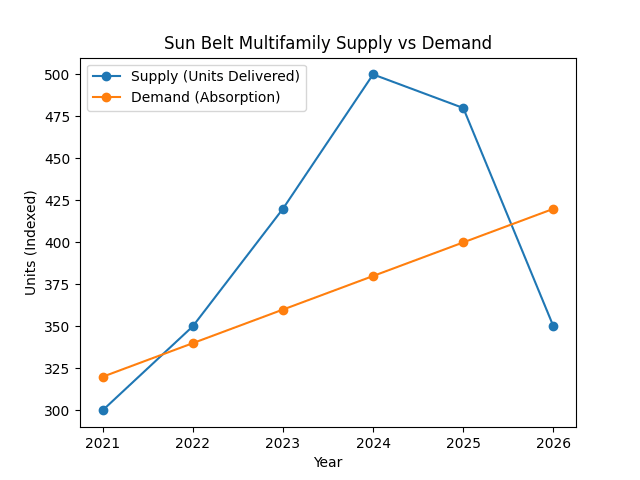

Supply vs Demand: The Real Driver of the Cycle

Why this matters:

This is the single most important macro driver of Camden’s business.

What it shows:

Recent years have seen supply (new apartment deliveries) exceed demand (absorption), which explains weak new lease pricing. However, the chart also shows that this imbalance is cyclical and begins to normalize as deliveries slow.

Bottom line:

Camden’s current weakness is not structural—it is cyclical. When supply slows, pricing power returns quickly.

Operating Leverage: Small Rent Changes, Large Earnings Impact

Why this matters:

This explains why the stock can move meaningfully even without strong top-line growth.

What it shows:

Small improvements in rent growth translate into disproportionately large increases in NOI due to the fixed-cost nature of multifamily operations.

Bottom line:

You do not need a housing boom—just a return to normal rent growth to drive earnings upside.

Scenario Analysis: Downside vs Upside

Why this matters:

This frames the investment as a probability-weighted outcome rather than a single forecast.

What it shows:

- Downside is limited if occupancy and cash flow remain stable

- Base case reflects normalization in rent growth

- Upside is driven by multiple expansion and improved sentiment

Bottom line:

The setup is asymmetrical—risk is contained, upside expands with normalization.

What Needs to Go Right

- New lease declines stabilize

- Renewal growth remains positive

- Supply deliveries slow meaningfully

- NOI returns to positive growth

- Market regains confidence in earnings stability

Why this matters:

This makes the thesis measurable and trackable over time.

Why the Opportunity Exists

Why this matters:

This explains why the market has not already priced in the recovery.

What it shows:

Investors are anchored to:

- negative new lease spreads

- weak near-term guidance

- oversupply headlines

They are not yet focused on:

- forward supply normalization

- embedded operating leverage

- stable cash flow and dividend coverage

Bottom line:

The market is backward-looking. The opportunity comes from looking one cycle ahead.

Bottom Line

Camden Property Trust is a high-quality multifamily REIT temporarily weighed down by a supply-driven rent slowdown.

The market is focused on:

- weak new lease rates

- muted near-term growth

But is underweighting:

- long-term demand

- portfolio quality

- cash flow durability

This is not a high-beta trade.

It is a cycle normalization trade.

DISCLAIMER

This analysis is not investment advice and reflects opinion only.

© 2026 MacroHint.com. All rights reserved.

This article is proudly sponsored by Lake Region State College.

Michael Lazenby

Editor-in-Chief, MacroHint

Michael Lazenby is the Editor-in-Chief and Founding Partner of MacroHint. He studied economics, business, and government at UT Austin and has hedge fund experience.