Johnson Controls International is reportedly weighing the sale of two businesses inside its security division — Access Control and Intrusion Detection — in a potential transaction that could be worth up to approximately $4.5 billion.

At first glance, this sounds like a normal corporate divestiture story.

It is not.

This is much more interesting than that.

Johnson Controls is a historically sprawling industrial conglomerate with businesses across HVAC, building systems, controls, fire safety, security, software, and commercial building infrastructure. For years, the company has had good assets, but not always a clean story. Investors have often struggled to answer a simple question:

What exactly is Johnson Controls supposed to be?

A commercial HVAC company?

A building automation company?

A fire and security company?

A data-center cooling beneficiary?

A software-enabled smart buildings platform?

A leftover industrial conglomerate?

The answer has usually been: a little bit of everything.

That is exactly what the company now appears to be trying to fix.

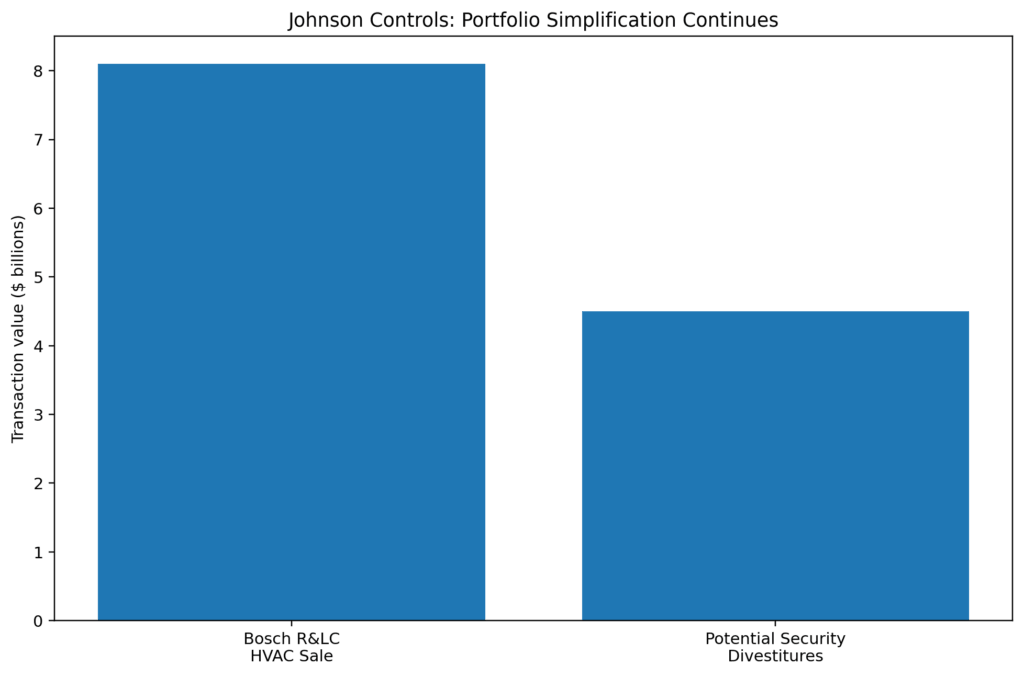

The potential sale of Access Control and Intrusion Detection would represent another step in Johnson Controls’ broader portfolio simplification effort, following the completed sale of its residential and light commercial HVAC business to Bosch in an approximately $8.1 billion transaction.

This is the real story:

Johnson Controls is trying to become simpler, cleaner, more commercial-building-focused, more service-heavy, and more worthy of a higher multiple.

Johnson Controls Security Asset Sale: The Situation

Johnson Controls is reportedly working with advisers to solicit interest for two units:

- Access Control

- Intrusion Detection

The businesses could be sold separately or together and may be worth up to approximately $4.5 billion.

Access Control focuses on systems that manage who can enter buildings, offices, campuses, and sensitive facilities. Intrusion Detection provides products such as sensors, detectors, alarms, and related security technologies to protect workplaces and commercial properties.

These are not bad businesses.

In fact, they are useful, recurring, mission-critical building-security assets.

But the real issue is whether they are the right assets for Johnson Controls to own if the company wants to become a more focused smart-buildings and commercial HVAC compounder.

Portfolio Simplification: The Bigger Story

Why this matters:

This chart shows that the potential $4.5 billion security divestiture would not be an isolated move. It would follow the much larger Bosch transaction, where Johnson Controls sold its residential and light commercial HVAC business.

What it shows:

Johnson Controls has already completed a major portfolio exit, and the potential security sale would continue the same strategic pattern: simplify the portfolio, exit less-core or lower-synergy businesses, and focus on higher-priority commercial building solutions.

Bottom line:

This is not random asset pruning. This is portfolio surgery.

Why This Matters

The market has already rewarded Johnson Controls.

The stock has gained significantly over the past year, and the company’s market value is now roughly in the mid-$80 billion range. That means investors are already pricing in some combination of:

- stronger execution

- cleaner portfolio

- data-center demand

- margin expansion

- activist-driven discipline

- new CEO credibility

- capital return potential

So the question is not whether Johnson Controls is improving.

It is.

The question is whether the improvement is already fully priced in.

That is where the potential divestiture becomes important. A $4.5 billion sale could give management more flexibility, but it also raises the bar. Once investors start paying for portfolio transformation, management has to deliver actual earnings quality improvement — not just press releases.

Company Overview

Johnson Controls is a global building-products and building-technology company. It provides HVAC systems, building controls, fire safety systems, security products, software, services, and integrated infrastructure for commercial buildings.

Its customers include:

- office buildings

- hospitals

- schools

- universities

- data centers

- industrial facilities

- airports

- government buildings

- commercial real estate owners

- large distributed enterprises

The company operates in an attractive long-term market because buildings are becoming more complex.

Modern buildings increasingly need:

- energy efficiency

- emissions reduction

- air-quality monitoring

- connected controls

- fire detection

- access management

- security monitoring

- data-center cooling

- predictive maintenance

- software-enabled building automation

That makes Johnson Controls more than a traditional industrial manufacturer. At its best, it is a building-infrastructure platform.

At its worst, however, it can look like a complicated industrial roll-up with too many product lines, uneven margins, and too much operational complexity.

The whole investment case depends on which version wins.

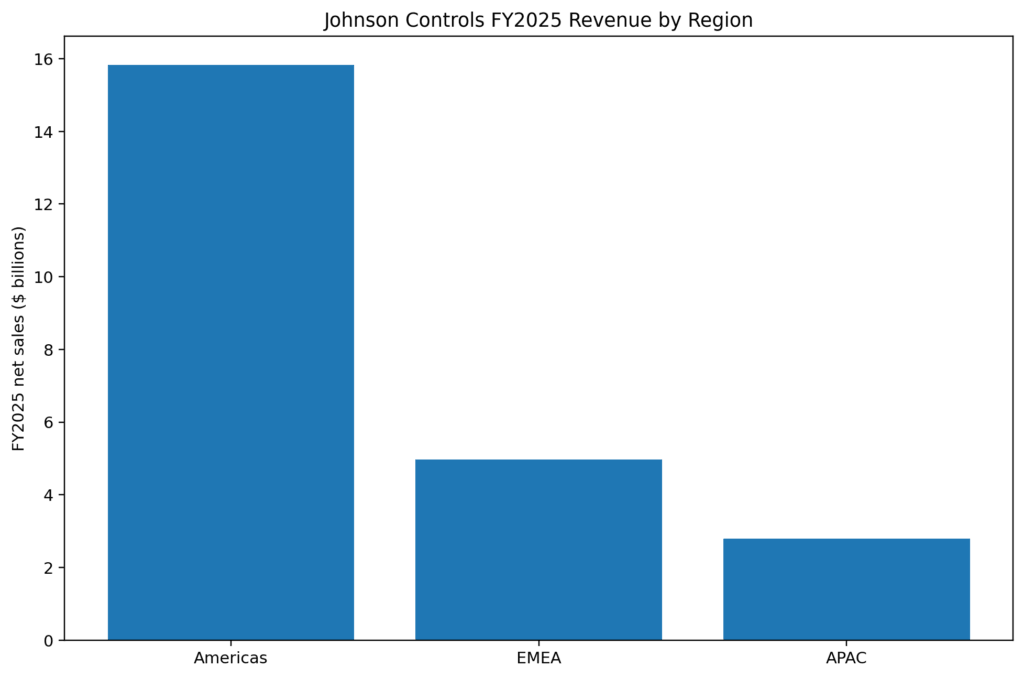

FY2025 Revenue Base

Why this matters:

This chart shows where Johnson Controls actually makes its money after the company’s portfolio realignment.

What it shows:

The Americas segment dominates the revenue base, followed by EMEA and APAC. In fiscal 2025, Johnson Controls reported approximately $15.8 billion of net sales in the Americas, approximately $5.0 billion in EMEA, and approximately $2.8 billion in APAC.

Bottom line:

Johnson Controls is primarily an Americas-driven commercial buildings company, not a perfectly balanced global conglomerate.

Segment Margin Profile

[INSERT IMAGE: jci_ebita_margin_by_region.png]

Why this matters:

Revenue alone does not tell the story. Margins show where the quality sits.

What it shows:

The Americas segment generates the largest profit pool and a strong EBITA margin. APAC also shows a solid margin profile, while EMEA is lower-margin. This matters because any portfolio simplification should ideally shift the company toward higher-margin, higher-quality, more scalable business lines.

Bottom line:

The opportunity is not just revenue growth. The opportunity is mix improvement.

What Johnson Controls Is Trying to Become

The company appears to be moving away from a “wide industrial product basket” model and toward a cleaner identity:

A commercial building technology platform focused on HVAC, controls, services, fire, safety, sustainability, and digital building management.

That matters because cleaner industrial companies usually receive higher valuation multiples.

Investors tend to reward:

- simpler business models

- recurring service revenue

- higher-margin mix

- clear end-market exposure

- measurable backlog

- pricing power

- strong free cash flow conversion

- focused capital allocation

Investors tend to discount:

- sprawling portfolios

- low-synergy business lines

- inconsistent margins

- complicated reporting

- unclear strategic identity

- hard-to-model cyclicality

Johnson Controls is trying to move from the second category into the first.

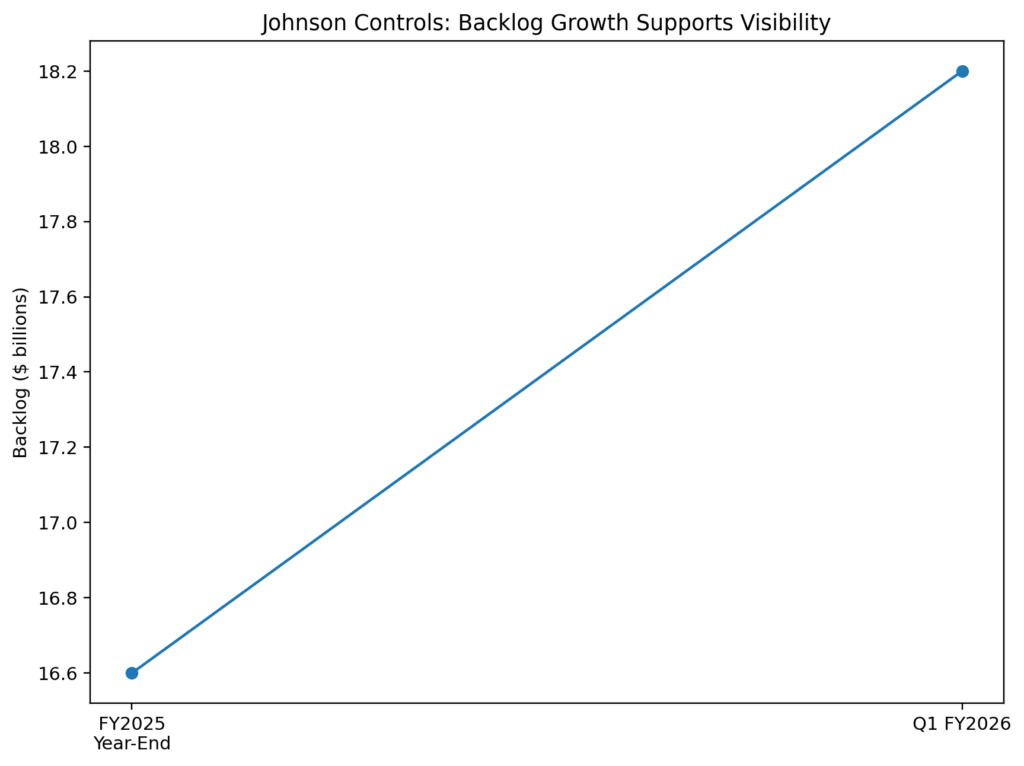

Backlog: Why Investors Are Paying Attention

Why this matters:

Backlog is critical because it gives visibility into future revenue. For an industrial and building-solutions company, backlog is one of the clearest indicators of demand.

What it shows:

Johnson Controls ended fiscal 2025 with a backlog of approximately $16.6 billion, and by Q1 fiscal 2026 reported backlog of approximately $18.2 billion. Orders also grew sharply in Q1 fiscal 2026.

Bottom line:

The market is not just buying a divestiture story. It is also buying a real demand story.

The Data-Center Angle

One of the most important reasons Johnson Controls has gained investor attention is its exposure to data-center demand.

AI infrastructure requires enormous amounts of power, cooling, monitoring, controls, and uptime reliability. Data centers need specialized systems to manage heat, airflow, safety, and building performance.

Johnson Controls benefits through:

- advanced cooling

- building automation

- controls

- fire detection

- security systems

- service and maintenance

- energy optimization

This matters because data centers are not ordinary buildings. They are mission-critical infrastructure. Downtime is extremely expensive, and performance requirements are much higher than in normal commercial buildings.

That gives suppliers like Johnson Controls a better demand backdrop, especially if they can provide integrated systems rather than standalone products.

This is also why portfolio simplification matters. If investors see Johnson Controls as a data-center infrastructure and smart-buildings company, the multiple can be higher. If they see it as a messy industrial conglomerate, the multiple should be lower.

Why Sell Access Control and Intrusion Detection?

At first, selling security assets may seem counterintuitive. Security is part of smart buildings. Access control and intrusion detection are clearly relevant to commercial infrastructure.

So why sell them?

There are several possible reasons.

1. They May Not Be Core Enough

Johnson Controls may believe its highest-return focus areas are HVAC, controls, services, decarbonization, and data-center-related building infrastructure.

Security products may be strategically adjacent but not central.

2. They May Be Better Owned by a Security Specialist

Access control and intrusion detection may command higher value in the hands of a buyer more focused on security platforms, alarm systems, identity management, or physical-security software.

A strategic buyer may be able to extract better synergies than Johnson Controls can.

3. The Company May Want to Simplify the Story

Investors want a clean narrative. Every non-core product line makes the story harder to understand.

Selling these units could help Johnson Controls tell a simpler story:

commercial buildings, HVAC, controls, services, data centers, sustainability.

4. The Valuation May Be Attractive

If the units can sell for up to $4.5 billion, Johnson Controls may be able to monetize them at an attractive multiple and redeploy proceeds into higher-return uses.

5. New Management May Want a Cleaner Operating Model

Joakim Weidemanis came from Danaher, a company known for operational discipline, portfolio focus, and business-system execution. It is not surprising that Johnson Controls under new leadership would review the portfolio more aggressively.

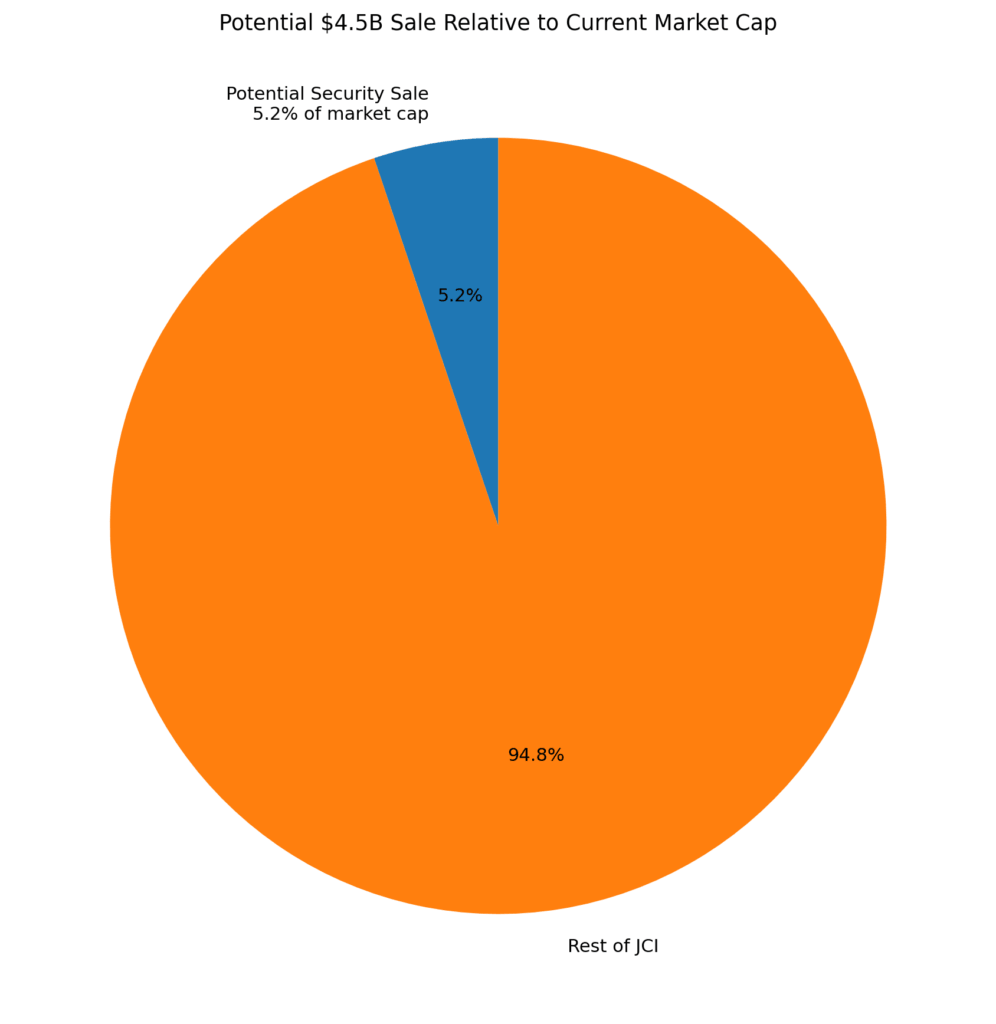

Potential Divestiture Relative to Market Cap

Why this matters:

This chart keeps the $4.5 billion number in perspective.

What it shows:

A $4.5 billion divestiture would be meaningful, but not transformational relative to Johnson Controls’ roughly $87 billion market capitalization. It is large enough to matter for capital allocation, but not large enough by itself to completely change the company.

Bottom line:

The strategic signal may matter more than the cash proceeds.

What Could Johnson Controls Do With the Proceeds?

If Johnson Controls sells the two security units for up to $4.5 billion, management could use proceeds for several purposes:

- share repurchases

- debt reduction

- tuck-in acquisitions

- investment in higher-growth platforms

- data-center cooling capacity

- digital building technology

- service expansion

- margin-improvement initiatives

The most attractive use depends on valuation.

If JCI stock is expensive, buybacks are less compelling. If management has high-return internal investments in data-center cooling, service platforms, or controls, reinvestment may be better. If leverage is a concern, debt reduction could improve resilience.

The best answer is probably a mix.

But the key is discipline. Selling a business at a good price only creates value if the proceeds are redeployed intelligently.

The Danaher Influence

The CEO angle is important.

Joakim Weidemanis previously worked at Danaher, which is one of the most admired industrial compounders in the market. Danaher is known for:

- portfolio discipline

- continuous improvement

- margin expansion

- decentralized accountability

- high-quality acquisitions

- focused execution

- business-system rigor

Investors naturally want to believe some of that DNA can transfer to Johnson Controls.

That is a powerful narrative.

But it can also become dangerous if expectations get too high.

Johnson Controls is not Danaher. It has different assets, different end markets, different margin structure, and different operational history. The correct bullish view is not “JCI becomes Danaher.” The more realistic view is:

JCI becomes a cleaner, more disciplined version of itself.

That is still valuable.

But investors should not confuse improvement with transformation.

Activist Pressure and Governance Reset

Johnson Controls has already gone through a governance and leadership reset after pressure from Elliott Investment Management. Elliott had built a major stake in the company, and the company subsequently moved toward leadership change, board refreshment, portfolio review, and simplification.

This matters because activist involvement often pushes companies to:

- exit non-core assets

- improve margins

- simplify reporting

- return capital

- sharpen strategic priorities

- accelerate management accountability

The potential security divestitures fit that pattern.

This is not just “management had an idea.”

This is part of a broader shareholder-value playbook.

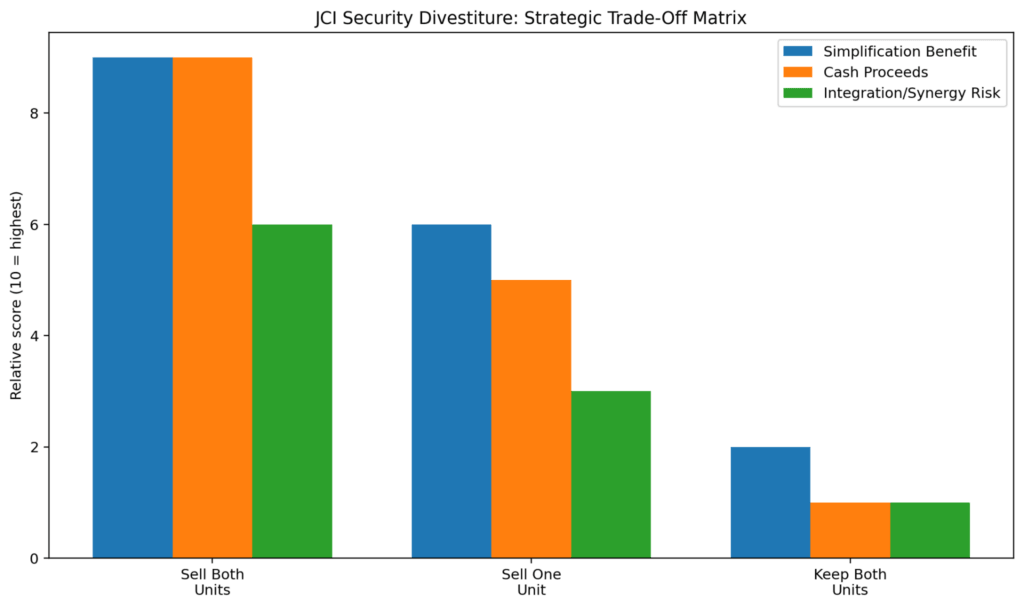

Strategic Trade-Off Matrix

Why this matters:

This chart shows the trade-off between selling both units, selling one unit, or keeping both.

What it shows:

Selling both units maximizes simplification and cash proceeds but creates the highest risk of losing integration or cross-selling benefits. Keeping both avoids disruption but does not help simplify the portfolio. Selling one unit is a middle path, but may not fully satisfy investors looking for a cleaner structure.

Bottom line:

The best financial decision may not be the same as the cleanest strategic decision.

Why the Units Might Attract Buyers

Access Control and Intrusion Detection are attractive because they sit inside a real long-term market: physical security.

Commercial buildings increasingly need:

- controlled access

- identity verification

- visitor management

- intrusion alarms

- connected sensors

- integrated monitoring

- hybrid physical/digital security

- compliance and audit trails

Potential buyers could include strategic security companies, building-technology firms, industrial automation companies, or private equity sponsors. These units may be especially attractive to buyers who can combine them with existing security platforms and extract cost or revenue synergies.

The buyer logic is simple:

Johnson Controls may view these businesses as non-core.

A focused buyer may view them as a platform.

That valuation gap is how divestitures create value.

But There Is a Real Risk

The risk is that security is more connected to smart buildings than the simplification narrative admits.

Modern buildings increasingly integrate:

- access control

- HVAC controls

- occupancy sensing

- energy management

- fire systems

- building automation

- emergency response

- workplace analytics

If Johnson Controls sells too much of the security stack, it may reduce its ability to offer fully integrated building solutions.

That is the subtle risk.

A cleaner company is not always a better company if the assets being sold are strategically useful.

This is why the deal perimeter matters.

Selling a product-heavy, lower-margin, less-integrated unit is one thing. Selling assets that strengthen the company’s integrated building platform is another.

Investors should watch exactly what is sold, what is retained, and whether Johnson Controls preserves software, integration, and service relationships.

Revenue Recognition and Business Model Mechanics

Johnson Controls generates revenue in several ways:

Product Sales

These include HVAC equipment, controls, fire-safety products, security hardware, sensors, and related systems. Product revenue is generally recognized when control of the product transfers to the customer.

Systems Revenue

This includes designed, installed, and integrated building systems. Revenue may be recognized over time depending on project structure and performance obligations.

Service Revenue

This includes maintenance, inspections, monitoring, repair, upgrades, and lifecycle support. This is often higher-quality revenue because it is more recurring and tied to installed base.

Backlog Conversion

Large building projects, data centers, commercial buildings, and infrastructure installations often enter backlog before revenue is recognized. This is why backlog matters.

The higher-quality Johnson Controls story depends on growing services and systems revenue relative to lower-margin or less-recurring product lines.

Cost Structure

Johnson Controls’ cost structure includes:

- raw materials

- components

- labor

- installation costs

- engineering

- field service technicians

- logistics

- warranty expense

- SG&A

- R&D

- restructuring costs

- amortization

- interest expense

The key operating leverage comes from:

- better backlog conversion

- price/cost discipline

- services mix

- factory productivity

- procurement savings

- portfolio simplification

- lower complexity

The portfolio simplification angle matters because complexity itself has a cost. A sprawling company needs more management layers, more systems, more reporting, more working capital, and more operational overhead.

Selling non-core assets can therefore create value even beyond the sale proceeds.

What the Market Is Pricing In

Johnson Controls currently trades at a premium valuation relative to where many old-line industrials historically traded. The market is not treating it like a broken conglomerate anymore.

That means investors are already expecting:

- margin expansion

- better execution

- data-center growth

- portfolio simplification

- disciplined capital allocation

- fewer restructuring distractions

This makes the setup more nuanced.

The stock may still work if management executes well, but the easy money from “obvious undervaluation” has likely already been made.

From here, the company has to grow into the story.

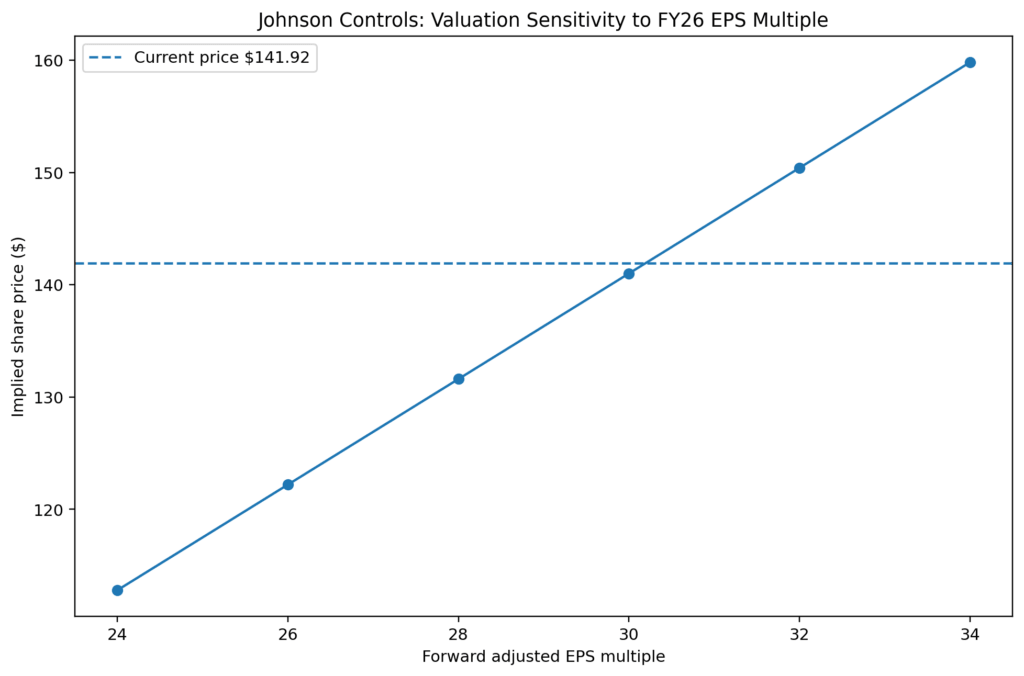

Valuation Sensitivity

Why this matters:

This chart shows how much of the stock’s value depends on the multiple investors are willing to pay.

What it shows:

Using a fiscal 2026 adjusted EPS midpoint of approximately $4.70, a 24x multiple implies roughly $113 per share, a 30x multiple implies roughly $141 per share, and a 34x multiple implies roughly $160 per share.

Bottom line:

At current levels, Johnson Controls already reflects a fairly optimistic multiple. Further upside likely requires continued backlog conversion, margin expansion, and confidence that portfolio simplification improves earnings quality.

Why Now?

This story matters now because several things are happening simultaneously:

- new CEO

- activist pressure

- portfolio review

- completed HVAC divestiture

- possible security divestitures

- strong backlog

- data-center demand

- higher valuation

- more scrutiny on execution

That combination creates an interesting setup.

Johnson Controls is no longer being valued like a sleepy industrial company. It is being valued like a company in transition.

The market is paying for improvement. The question is whether management can deliver enough improvement to justify that price.

Stock Pitch: Johnson Controls International (NYSE: JCI)

Executive Summary

Johnson Controls is becoming a cleaner, more focused commercial building technology company. The potential $4.5 billion divestiture of Access Control and Intrusion Detection would continue a broader simplification strategy already demonstrated by the sale of the residential and light commercial HVAC business to Bosch.

The company has strong backlog, exposure to data-center cooling and smart buildings, activist-driven discipline, and a new CEO with Danaher experience.

However, the stock has already re-rated significantly. That means this is not a screamingly cheap special situation. It is a quality-improvement story where future upside depends on execution.

Rating: Hold / Watchlist with upside if execution remains strong

This is a company to respect, not chase blindly.

Upside Drivers

1. Portfolio Simplification

Selling non-core assets can improve margins, reduce complexity, and make the business easier to understand.

2. Data-Center Demand

AI infrastructure requires cooling, controls, fire safety, monitoring, and building automation. Johnson Controls is positioned to benefit from this spending cycle.

3. Backlog Conversion

A large backlog creates revenue visibility. If backlog converts at attractive margins, earnings can continue compounding.

4. Service Mix

More service revenue improves stability, cash flow quality, and valuation multiple.

5. Capital Allocation

Divestiture proceeds can support buybacks, reinvestment, debt reduction, or targeted acquisitions.

6. Operational Discipline

New leadership may drive a more disciplined operating culture and sharper margin focus.

What Would Break the Thesis?

The thesis would weaken if:

- the security units sell for less than expected

- divestiture proceeds are poorly redeployed

- data-center demand slows

- backlog converts at lower-than-expected margins

- service growth disappoints

- the company loses too much integrated building capability

- valuation multiple compresses

- restructuring creates disruption instead of simplicity

The biggest risk is not that Johnson Controls is a bad company.

The biggest risk is that it is now a good company priced like a great one.

Competitive Positioning

Johnson Controls competes across building technology, HVAC, controls, fire, safety, and security against companies such as Honeywell, Carrier, Trane Technologies, Siemens, Schneider Electric, ABB, Allegion, Assa Abloy, and others depending on the product category.

Its competitive advantages include:

- large installed base

- global customer relationships

- service network

- building systems expertise

- data-center exposure

- broad product portfolio

- controls and automation capabilities

Its weaknesses include:

- portfolio complexity

- uneven margin history

- execution risk

- exposure to cyclical construction markets

- potential strategic dilution if it sells too many connected assets

The strategic challenge is to become focused without becoming less complete.

That is harder than it sounds.

Capital Allocation

If Johnson Controls receives up to $4.5 billion from the potential security divestitures, the company has several options:

- repurchase shares

- reduce debt

- invest in organic growth

- expand data-center and cooling capabilities

- pursue targeted acquisitions

- improve digital/software platforms

- support restructuring and productivity programs

The best outcome would be disciplined redeployment into higher-return areas.

The worst outcome would be selling good assets and using the proceeds to buy back expensive stock or pursue mediocre acquisitions.

Capital allocation will determine whether this deal creates value.

Current Market Sentiment

The market currently views Johnson Controls as:

- a cleaner company than before

- a beneficiary of data-center demand

- an activist-influenced self-help story

- a potential margin expansion story

- a higher-quality building technology platform

That is a much better narrative than the company had a few years ago.

But the sentiment is no longer depressed.

This matters because improved sentiment reduces margin of safety.

What Needs to Go Right

For the stock to keep working, several things need to happen:

- Access Control and Intrusion Detection must sell at attractive valuations

- proceeds must be redeployed intelligently

- backlog must convert into revenue at strong margins

- data-center demand must remain durable

- service revenue must keep growing

- management must reduce complexity without damaging cross-selling

- margins must continue improving

- the market must keep rewarding JCI with a premium multiple

This is no longer just a “simplify the portfolio” story.

It is now an execution story.

Why the Opportunity Exists

The opportunity exists because Johnson Controls sits in a powerful intersection:

- commercial building modernization

- energy efficiency

- AI data-center infrastructure

- sustainability spending

- security and safety needs

- portfolio simplification

- activist discipline

That is a very attractive mix.

But the stock already knows that.

So the real opportunity is not buying a hidden gem. It is identifying whether the market is still underestimating the magnitude of operational improvement under the new strategy.

That is a much more subtle thesis.

Bottom Line

Johnson Controls’ potential $4.5 billion sale of Access Control and Intrusion Detection is not just a divestiture story.

It is another step in a broader attempt to transform JCI from a sprawling industrial conglomerate into a cleaner, higher-quality, higher-multiple commercial building technology company.

The strategic logic makes sense:

- simplify the company

- focus on commercial building solutions

- emphasize services and systems

- lean into data-center demand

- improve margins

- redeploy capital

But the valuation is no longer cheap.

The stock has already moved significantly, and investors are already rewarding the transformation story.

That means the right conclusion is balanced:

Johnson Controls is becoming a better company, but the stock increasingly requires proof.

If management executes, the divestiture could be another positive step toward a cleaner, higher-quality business.

If execution disappoints, the market may realize it paid too early for a transformation that still has to be earned.

DISCLAIMER

This analysis is not investment advice and reflects opinion only.

© 2026 MacroHint.com. All rights reserved.

This article is proudly sponsored by Lake Region State College.

Michael Lazenby

Michael Lazenby is the Editor-in-Chief and Founding Partner of MacroHint. He studied economics, business, and government at UT Austin and has hedge fund experience.

Michael Lazenby is the Editor-in-Chief and Founding Partner of MacroHint. He studied economics, business, and government at UT Austin and has hedge fund experience.